All Categories

Featured

Table of Contents

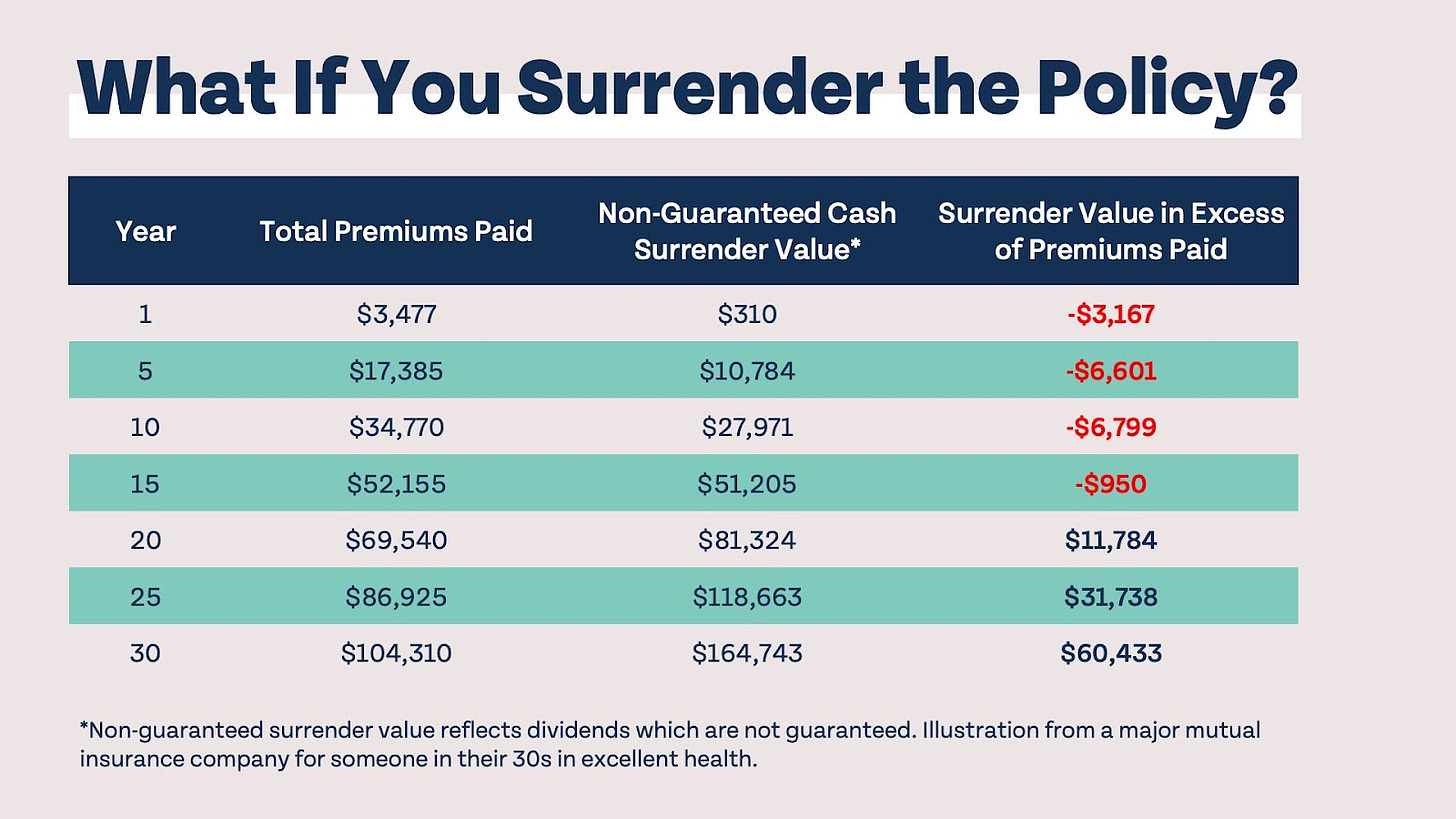

For many people, the greatest problem with the limitless banking concept is that first hit to early liquidity brought on by the expenses. This disadvantage of infinite banking can be reduced considerably with correct policy layout, the first years will always be the worst years with any kind of Whole Life plan.

That stated, there are specific limitless financial life insurance policy plans created primarily for high early money value (HECV) of over 90% in the first year. Nevertheless, the lasting efficiency will frequently significantly delay the best-performing Infinite Banking life insurance policy policies. Having accessibility to that extra four figures in the very first few years may come with the cost of 6-figures in the future.

You actually get some substantial long-term advantages that aid you recover these early costs and after that some. We find that this prevented early liquidity problem with boundless financial is more psychological than anything else as soon as completely discovered. Actually, if they definitely required every cent of the cash missing from their boundless financial life insurance policy policy in the first few years.

Tag: limitless banking idea In this episode, I talk about financial resources with Mary Jo Irmen that instructs the Infinite Banking Principle. With the surge of TikTok as an information-sharing platform, financial advice and techniques have actually found a novel way of dispersing. One such strategy that has actually been making the rounds is the unlimited financial concept, or IBC for short, amassing recommendations from stars like rap artist Waka Flocka Fire.

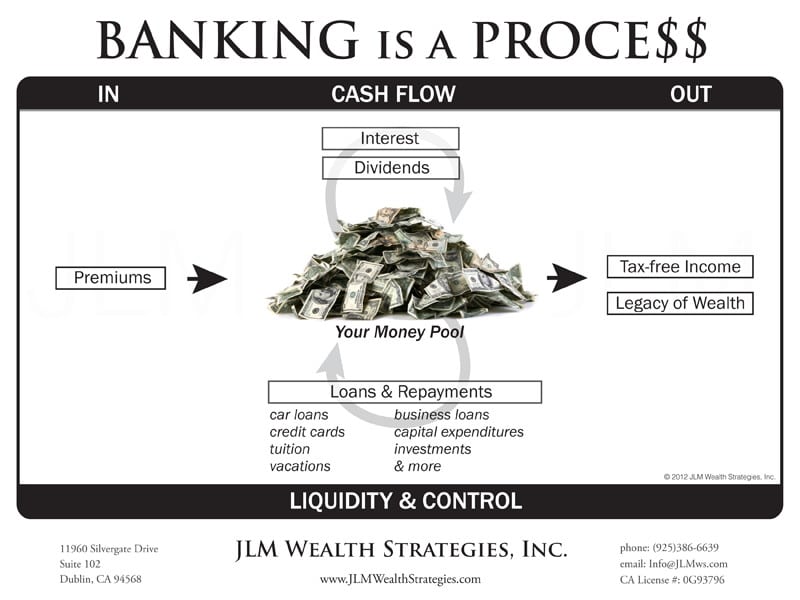

Within these policies, the money worth grows based upon a price set by the insurance company. When a significant money value collects, insurance holders can get a cash worth loan. These loans vary from conventional ones, with life insurance policy functioning as collateral, meaning one could shed their insurance coverage if borrowing excessively without appropriate cash value to sustain the insurance policy costs.

And while the allure of these plans is obvious, there are innate limitations and threats, demanding diligent cash worth monitoring. The technique's legitimacy isn't black and white. For high-net-worth individuals or entrepreneur, particularly those using methods like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and substance development could be appealing.

Infinite Banking Institute

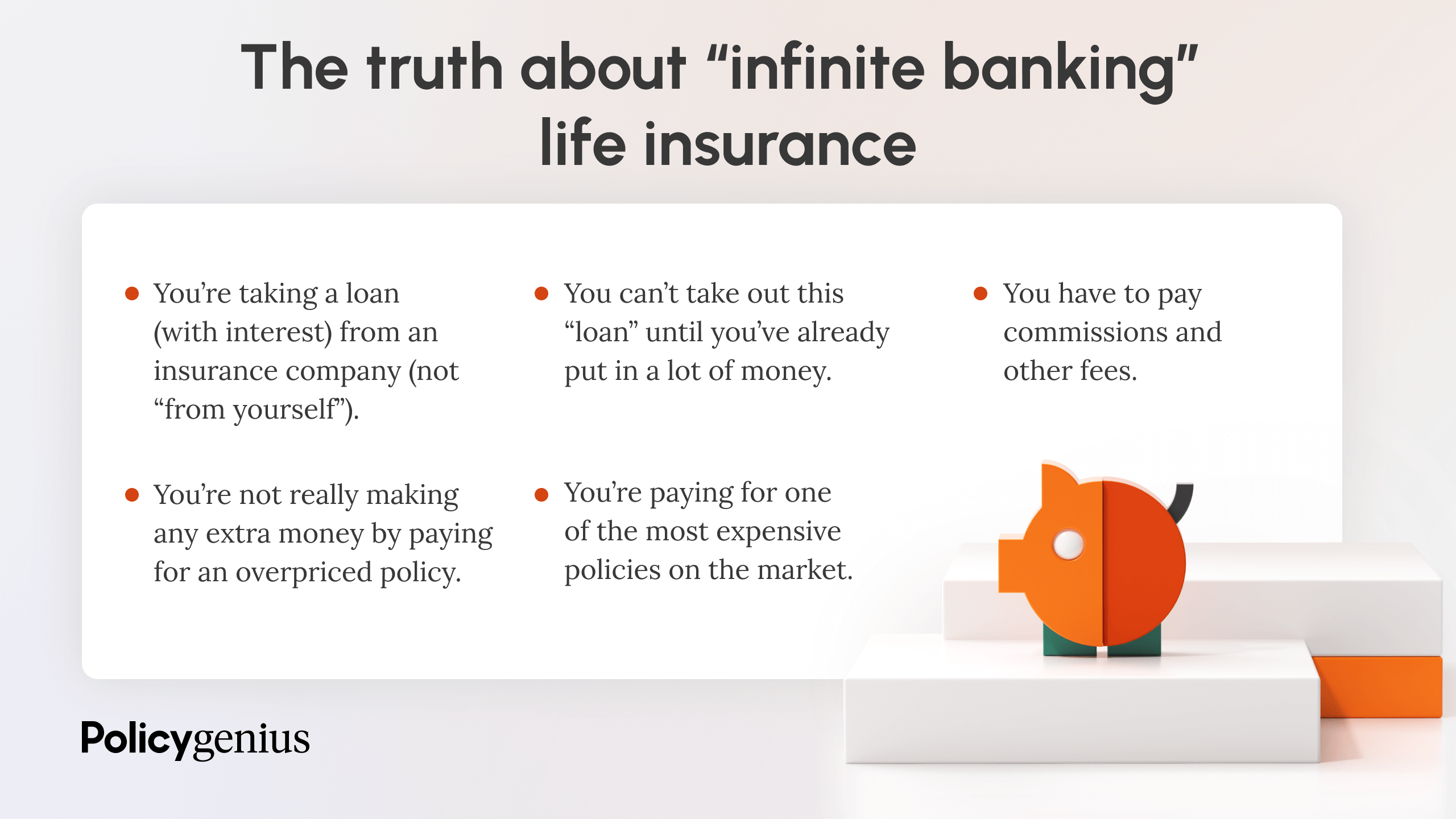

The allure of boundless banking does not negate its difficulties: Cost: The fundamental demand, an irreversible life insurance coverage policy, is more expensive than its term equivalents. Eligibility: Not everybody gets approved for entire life insurance policy because of rigorous underwriting processes that can exclude those with particular wellness or lifestyle conditions. Complexity and danger: The detailed nature of IBC, coupled with its risks, may deter many, especially when less complex and much less high-risk options are offered.

Designating around 10% of your monthly income to the policy is just not viable for the majority of people. Utilizing life insurance policy as an investment and liquidity resource calls for technique and monitoring of policy cash worth. Consult an economic expert to determine if unlimited banking lines up with your top priorities. Part of what you read below is simply a reiteration of what has actually currently been said over.

So prior to you obtain into a situation you're not prepared for, know the following first: Although the idea is commonly sold as such, you're not in fact taking a funding from on your own. If that were the case, you wouldn't need to repay it. Rather, you're obtaining from the insurance provider and have to repay it with passion.

Some social media blog posts suggest making use of money worth from whole life insurance to pay down credit rating card debt. When you pay back the car loan, a portion of that rate of interest goes to the insurance company.

For the first several years, you'll be paying off the compensation. This makes it exceptionally challenging for your policy to build up worth during this time. Unless you can manage to pay a couple of to several hundred bucks for the next decade or more, IBC will not function for you.

Royal Bank Visa Infinite Avion

Not every person needs to count entirely on themselves for financial security. If you require life insurance, right here are some important suggestions to think about: Think about term life insurance policy. These plans give insurance coverage during years with significant financial responsibilities, like mortgages, trainee fundings, or when taking care of kids. See to it to look around for the very best rate.

Copyright (c) 2023, Intercom, Inc. () with Scheduled Typeface Call "Montserrat". This Typeface Software is accredited under the SIL Open Up Font Style Certificate, Version 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Font Style Call "Montserrat". This Typeface Software is licensed under the SIL Open Up Font Style License, Variation 1.1.Avoid to primary content

Infinite Banking Illustration

As a CPA focusing on property investing, I have actually combed shoulders with the "Infinite Financial Idea" (IBC) extra times than I can count. I have actually also talked to experts on the subject. The major draw, other than the apparent life insurance policy advantages, was always the idea of developing money value within a permanent life insurance policy policy and loaning against it.

Sure, that makes sense. But honestly, I constantly thought that cash would be better invested directly on financial investments instead of channeling it through a life insurance plan Till I found how IBC can be combined with an Irrevocable Life Insurance Policy Count On (ILIT) to produce generational riches. Allow's begin with the essentials.

Infinite Banking Uk

When you obtain against your plan's cash value, there's no set repayment schedule, offering you the freedom to manage the lending on your terms. Meanwhile, the cash money value remains to grow based on the plan's assurances and rewards. This arrangement allows you to accessibility liquidity without interrupting the long-term growth of your plan, supplied that the finance and rate of interest are managed intelligently.

The procedure continues with future generations. As grandchildren are birthed and expand up, the ILIT can buy life insurance policies on their lives. The trust fund then collects several plans, each with growing cash money values and death benefits. With these policies in area, the ILIT successfully comes to be a "Family Bank." Relative can take fundings from the ILIT, using the cash money worth of the policies to money investments, start companies, or cover significant expenses.

An essential element of managing this Family members Bank is the use of the HEMS standard, which means "Wellness, Education, Upkeep, or Assistance." This guideline is often consisted of in count on arrangements to guide the trustee on just how they can disperse funds to recipients. By sticking to the HEMS standard, the count on guarantees that circulations are made for necessary needs and lasting support, safeguarding the trust's assets while still offering for household participants.

Enhanced Flexibility: Unlike inflexible small business loan, you manage the settlement terms when borrowing from your very own plan. This enables you to framework settlements in such a way that aligns with your organization money flow. is infinite banking a scam. Enhanced Money Flow: By financing organization expenditures with plan finances, you can potentially liberate money that would otherwise be linked up in traditional lending repayments or tools leases

He has the very same devices, however has likewise built extra money worth in his plan and obtained tax benefits. Plus, he currently has $50,000 readily available in his plan to make use of for future opportunities or expenditures. In spite of its prospective advantages, some people remain cynical of the Infinite Financial Idea. Allow's address a couple of common concerns: "Isn't this just pricey life insurance policy?" While it holds true that the premiums for a properly structured entire life policy may be higher than term insurance coverage, it is very important to watch it as greater than just life insurance policy.

Infinite Banking Nelson Nash

It has to do with creating an adaptable financing system that offers you control and gives multiple advantages. When used purposefully, it can enhance other financial investments and business strategies. If you're intrigued by the potential of the Infinite Banking Idea for your service, right here are some steps to consider: Inform Yourself: Dive deeper into the concept through trusted books, seminars, or examinations with experienced experts.

{kind=link}

Latest Posts

Infinite Banking Explained

What Is Infinite Banking Life Insurance

Alliance Bank Visa Infinite Priority Pass